家計の税負担率とは?

この風刺画について

この風刺画「家計の税負担率」は、現代の一般家庭がどれほど税金に圧迫されているかを、視覚的にわかりやすく示すことを目的として制作しました。

インフレや物価高騰、光熱費の値上げなど、生活に直接影響を与える要因が増える一方で、「気づかないうちに増えている税負担」について、一般市民がどれほど把握しているのかという疑問から出発した作品です。

TOPの風刺画は3つで構成されています。

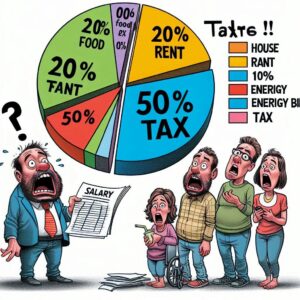

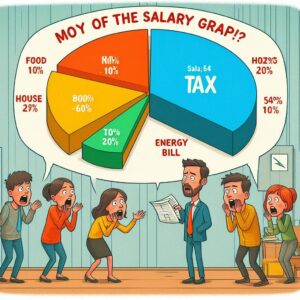

左から順に、給与明細を見て驚く男性と、その背景に「税金が50%を占める家計の内訳」。

中央では、実際の出費と税金を計算した結果に愕然とする家族たちの姿。

右の風刺画では、家賃や光熱費なども「税」の一種として認識され始め、「全てが税金に見えてしまう」錯覚に陥った人々の混乱を描いています。

一見、ユーモラスな表情や鮮やかな円グラフに目を引かれますが、実際には社会に対する鋭い問いかけが込められています。

「給与明細に書かれた税額だけが本当の負担なのか?」、「税金という名目でなくても、家計を圧迫する制度が他にもあるのでは?」という問題意識を視覚化しました。

私はこの風刺画で、複雑で見えにくくなっている現代の「見えない増税」をテーマにしました。

視覚的に「これはおかしい」と直感的に気づいてもらうことを狙っています。

家計の中で何が本当に「必要な支出」で、何が「制度的に過剰な負担」なのか。

この問いに多くの人が向き合うきっかけとなれば嬉しいです。

風刺画のポイント

この風刺画を描く際、特にこだわったのは「税金の可視化」と「家計感覚とのギャップ」を浮き彫りにすることです。

実際、税金というのは所得税や消費税だけでなく、社会保険料やエネルギー価格に内包された環境税、通信費に含まれる電波利用料など、目に見えない形で広く分散しています。

そのため、単なる「税額一覧」では伝わらない「生活者の感覚」と「制度の現実」とのズレを、ビジュアルで表現したかったのです。

左の風刺画では、グラフ内の「20% FOOD」「20% FANT(FUNのパロディ)」「50% TAX」といった極端な分布を描くことで、視覚的にすぐ「税金が高すぎる」と気づいてもらえるようにしました。

また、「FANT」という謎の表記を使ったのは、消費者自身が何にお金を使っているかすら曖昧になっている現代を象徴させるためです。

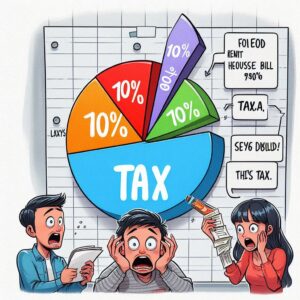

中央の風刺画では、どんな家庭でも一度は経験する「家計簿チェックでの衝撃」を描いています。

その顔のリアクションやグラフ上の「意味不明な英語(TAXA、LAXYS、SEY6 DBLUD)」は、制度が複雑化しすぎて理解できなくなっていることを皮肉っています。

これは現代の税制や補助金制度が、誰にでも理解できるようには設計されていないという事実への批判です。

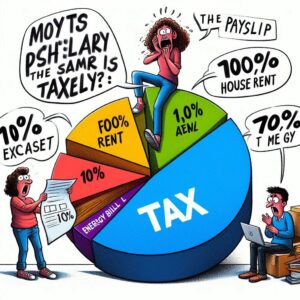

最後の右の風刺画では、いよいよ家計の崩壊を象徴的に描いています。

「100% HOUSE RENT」や「1.0% AEWL(意味不明な支出項目)」など、もはや何が税で何が生活費なのかすら曖昧になってしまう現象を表しています。

一人の女性が「THE PAYSLIP」と叫びながらグラフにしがみついている構図は、「明細書ですら救いにならない」現実を風刺しています。

このように、私は風刺画をただの皮肉で終わらせたくないと考えています。

むしろ「問題の見える化ツール」として活用できるアートであるべきだと信じています。

誰もが感じているけれど、うまく言語化できない違和感や不満。

それをビジュアルに落とし込み、笑いと驚きの中に「本質」を潜ませる。

それが私の風刺画制作の信条です。

この作品が「税金の見え方」を変えるきっかけとなれば、制作者としてこれ以上の喜びはありません。

AIが描いた「家計の税負担率」

|

|

|

|

|

|

|

コメント